")

It has been precisely a year since Gearbox V2 was released. Leveraged LPing, leveraged staking, and other initiatives have been available for a year now. A year has passed since Gearbox TVL rose to $100M+ in just three days, showcasing to the world the potential of capital-efficient credit. However, that was all a year ago; what counts now is what we accomplish today. And for that reason, we present to you Gearbox V3 in our continuing effort to create something deserving of evolving onchain credit.

Gearbox V2 tested the first Onchain Credit application, while Gearbox V1 served as a production test for Gearbox’s credit accounts. To build a protocol that works as a Credit Layer in DeFi, NFTs, RWA, and other contexts is the aim of Gearbox V3. a credit protocol that can generate a variety of credit products with an emphasis on increased capital efficiency and untapped market segments.

This article is broken up into three main sections, which are explained below. Get started!

Section 1: The story of credit and its existence

Section 2: Narrative wars and lending architectures

Section 3: Details of V3 and the new core protocol

Section 1: Creating the Scene.

1 Is Looping vs. Perps = Leverage = Credit?

Let’s retrace our steps and discuss Credit in DeFi, NFTs, RWA, and other related topics. What qualifies as a credit? Basically, credit is “more capital so you can do what you want.” For instance, you wish to increase your exposure to the upside of ETH. There are several methods for doing this:

- Borrow-lend swapping-looping on lending protocols such as Aave, where trades are executed using the available DEX liquidity;

- utilizing perpetuals on CEXs that make use of their own orderbooks and liquidity, such as Binance or OKX;

- utilizing perpetual DEXes with potentially thin liquidity, such as GMX or dYdX, which make use of their own orderbooks;

- By using Gearbox’s margin trading feature, which makes use of the DEX’s current liquidity,

Therefore, these can all essentially mean the same thing to a user who just wants to get “more exposure to a given asset”: credit, leverage, perpetuals, and futures. For example, in the real world, there are several ways to learn about “Spanish Real Estate.” ReITs, physical purchases, additional synthetic exposure, and so forth. Although the path is very different, the outcome may be similar And it is that path that determines the user experience, or UX.

We’ve gone into greater detail in our writing about the what and how of Onchain Credit. highlighting the nature and purpose of credit, its historical evolution, and the reasons capital efficiency is Onchain Credit’s logical next step. You’re literate.

1.2 Credit Account {abstraction} Powered

By providing each person with their own “Credit Account” through account abstraction, Gearbox is addressing the subject of credit (leverage) from the perspective of the best possible user experience. It can be thought of as having a leveraged wallet of its own. All you have to do is acquire additional funds and apply them to the protocols you already adore.

Even though we wrote about this topic more than two years ago, it is still relevant today. Hey, it’s account abstraction! Nothing of the kind, no vaults, no locking times, no one holding you back. At Gearbox, user autonomy is paramount!

Anyone can be a user of Gearbox—a human, a bot, a protocol, etc. Being a Credit Layer in between each participant is the aim of the Gearbox Protocol. Using PURE spot liquidity in all farming and trading activities rather than replicating liquidity like perps.

Do you recall credit cards? Because of their extensive network, you are able to use it anywhere to make payments. Similarly, picture being able to ape with more capital on any protocol because of Gearbox’s onchain credit. We have been constructing that since the year 21 and right now V3 has brought us one step closer to reality!

Section 2: Architectural Choices and Story Conflicts

We started working on new collateral integrations as soon as V2 was released in 2022, and we stopped there. Increasing the credit primitive entails answering extremely private security questions. Prior to delving into remedies, let us examine the wider context.

A few protocols (Morpho, Ajna, Euler, etc.) have investigated ways to make lending a less sophisticated primitive in the last year. Absence of risk granularity, governance, etc. Aave, meanwhile, illustrates the advantages of hand-holding for end users. It’s also true that users would prefer to simply receive a “good APY low risk,” whatever that may entail, rather than actually bothering with all these little details.

The Gearbox Protocol is composed and modular. It doesn’t adopt a position on this narrative conflict. It must be as comprehensive as possible as a protocol. V3 is therefore predicated on:

2.1 Composability and Modularity

The goal of V3 was to divide all the tasks associated with the protocol’s operation into modules, as we have been doing since 2021. This makes it possible for individual parts to be used in various settings while still fulfilling Gearbox’s needs when combined. This makes it possible for future integrations to have much more flexibility:

Better Composability: using more oracle sources instead of just Chainlink, and being able to incorporate and add adapters into new protocols and assets more quickly;

Better Risk Granularity: the ability to include those fascinating credit opportunities without raising protocol risks and allowing lenders to choose the level of risk they take on.

As much as you like, you can reconnect modular pieces to essentially increase or decrease risk, as well as choose which assets and LTVs to use! Gearbox V2 made this possible already, but we improved upon it.

- Imagine a different risk pool, where lenders can choose to earn higher yields while remaining passive and indirectly exposed to more upscale assets.

- One could envision a different DAO Treasury with “its own gearbox,” wherein THEIR governance determines the LTVs and the AllowedList, thereby setting their own prices for risks.

Think of KYC “narctech” pools with restricted lists, which function similarly to Leverage Ninja lists but with different TCR terminology.

2.2 Security and Risk

Onchain dark forests carry a number of known and unknown risks, as usual. Although Gearbox has never had any bad debt to date, you never know when danger might strike. As a result, every hour, the majority of the efforts are directed toward security.

First off, in advance of the deployment in a few days, V3 will be added to the audit repository after completing a thorough audit by ChainSecurity and ABDK. However, there are always more audits needed, so the following other initiatives are ongoing in parallel:

Both Immunefi and Bug Bounty have paid out a few respectable amounts thus far. Therefore, if you work as a security researcher, remember that we are always grateful to collaborate and will compensate you well!

We have created a massive backend monitoring tool that examines model liquidations, oracle deviations, and collateral health. not only for Gearbox but for every resource and protocol we’ve incorporated. In order to gain access and construct it further with us, don’t hesitate to ask!

Section 3: V3 Gearbox Protocol

- Limits on collateral for L2 deployments and new assets

- Particularly Risky Lending Pools

- ERC4626 tokens for diesel

- partial withdrawals of collateral

- Onchain bots known as intent agents, or gearbots

- Lending rates, gauges, and quotas

- GEAR’s Minimum Viable Tokenomics and Revenue Sources

3.1 Limits on collateral

Recall the concerns this year regarding CRV vs. lending protocols? Everyone could see that we were seeing through them, and in order to add new farms and chains, we had to make improvements to the codebase. Because even something as liquid as WBTC on rollups has a limited amount of liquidity. As a result, even for the ostensibly large assets, you must set collateral limits.

It goes without saying that governance sets the boundaries. Thus, Gearbox can expand in numerous additional ways thanks to this method:

Addition of medium- and long-tail assets: By restricting the exposure, Gearbox is able to add these assets and broaden its leverage.

Deploying on L2s: Consequently, it also becomes feasible to deploy on L2. The side chains and L2s suffer from reduced liquidity, which could become an increasingly serious issue as the multichain expands or contracts.

Capped at $1–2 million, new cool protocols and asset classes (which typically have low liquidity, high risk, but also large yields) can be added. insignificant in comparison to the lending pools that are currently in place, but it can be a great way to maintain leadership and encourage the more recent DeFi entrants. Haha!

3.2 Lending Pools Particular to Risk (Alpha)

Gearbox wants to increase the number of protocols and resources that users can access, so the DAO will begin looking into alternatives to the existing high-quality integrations. Curve V2 pools, a more recent integration, are a little more erratic. Due to this volatility, there is a slight increase in risk; therefore, interest rates should rise along with risk.

3.3 The passive end Diesel tokens

will eventually become ERC4626 Diesel tokens represent a depositor’s portion of a vault—in our case, a lending pool. Cheaper, simpler, and better for external integrations

There are a ton more lending categories with a wide range of variables that could be growth drivers. Gearbox is more modular than it has ever been, allowing you to dive into more niche markets. The pools below are not a sign of impending additions, but rather examples of what could all be made possible. Everybody is liable to DAO voting.

3.4. Reductions in part

Partial withdrawals were not previously allowed due to additional security concerns, but we enabled this feature because it is very important. When they receive rewards, a lot of farmers in particular want to take the money out without touching the underlying. In the same way that dividend ETFs differ from double-down ones. Just different tools, but both should be supported by the protocol.

Consequently, partial collateral withdrawal will be available in V3, rather than just debt reduction as it was in the past. Users should find it quick enough as it will be in some sort of withdrawal period mode that lasts less than 24 hours! And just in case, with a few additional security precautions in place.

3.5. Intent Agents in Gearbots UX

It’s also critical to ensure that the UX keeps improving in between all of the enhancements. We used Multicall to do that last year. Account abstraction was used by Multicall to group transactions and enable one-click communication between several contracts. Yes, complex farms with just one click!

Bringing true automation onchain to life, which allows you to use leverage and have a CEX-like experience, is the next step in our quest for better UX. What? – Introducing the Gearbots, our intent agents.

With the help of open source, unchangeable automation contracts called “gearbots,” CA owners can effectively assign some responsibilities related to active account management to an impartial, third party. One way to accomplish this would be to use Gelato Network to initiate the implementation of a smart contract’s reasoning. The user defines the logic itself, and smart contracts make sure the logic operates within the parameters that have been set.

3.6. GEAR staking: Quotas and Gauges

Limits on collateral apply to the entire protocol—that is, Credit Managers. See them as “anything beyond that number is ignored as collateral; the protocol/pool is not exposed to CRV beyond $3X total value of CRV.” This has a clear benefit, as stated in 3.1 above. The amount is set by governance and serves as a more tangible value that probably changes infrequently. Some things underneath are more likely to change.

Come on, quotas. Each leverage user sets aside a certain amount of money, saying, “How much of any X collateral asset on my Credit Account I want to go towards the total Health Factor.” As much as possible, of course. Consider it a technical implementation, though, in any case. More specifically, at the contract level, it facilitates a more democratic distribution of limited collaterals amongst leverage users.

When you use leverage, you basically borrow a debt asset (like USDC) and designate what you want it to be used for—a trade, a farm, or anything else. Because of this, the protocol can determine how much more to charge you based on whether or not you are in a risky asset. It goes very smoothly!

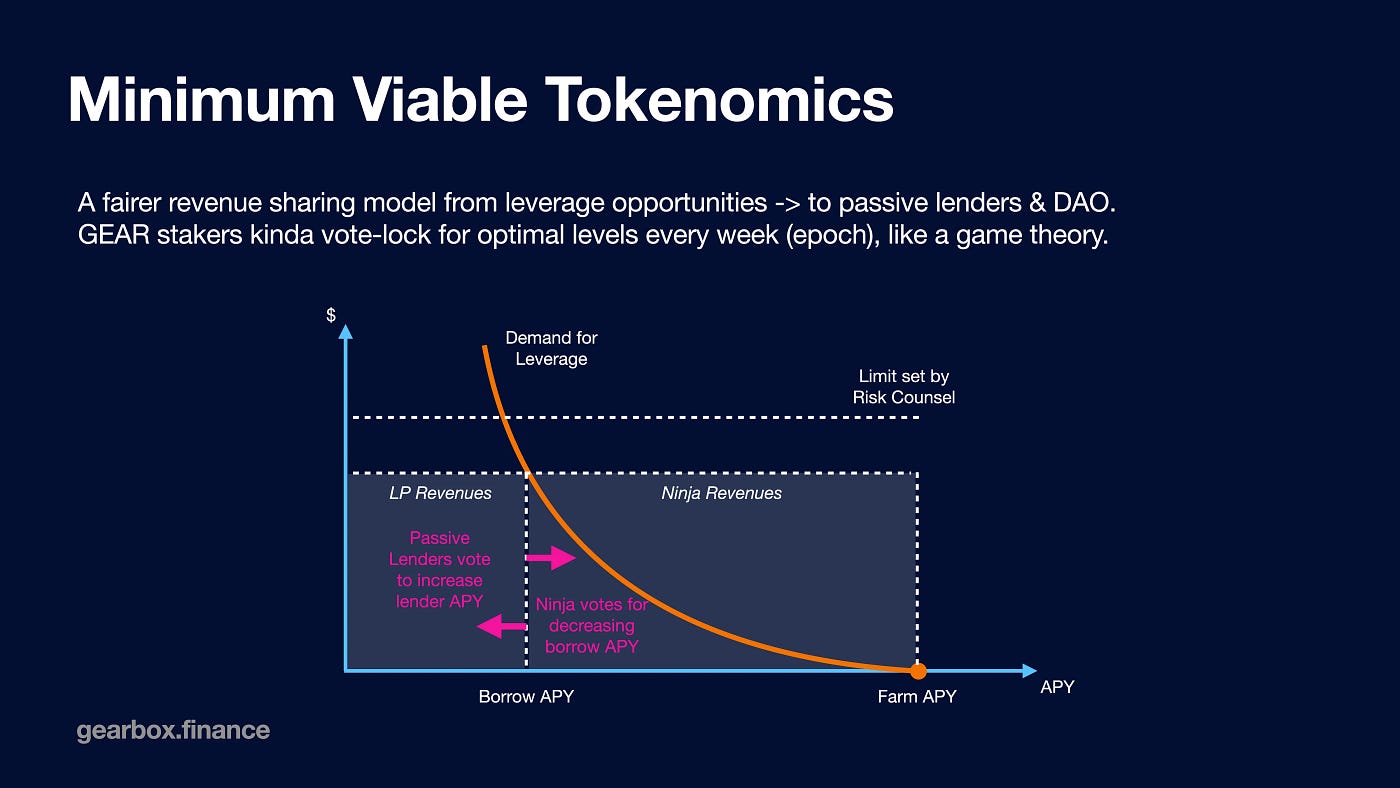

What? An additional bill? Indeed, sir. Gauges, enter. These are entirely different from the inflationary gauges in Curve, nono. Gauges are essentially a tool for calculating “what extra APY rates are paid by a borrower every epoch, on top of the usual utilization curve, for each asset separately” (an epoch is typically seven days long, but it can be longer). This is essentially how the protocol bills extra for quotas.

The tools used to determine how much is paid for each quota are called gauges. To protect themselves from attacks on governance, GEAR stakers freeze their tokens before casting their votes.

3.7. Tokenomics at Minimum Viability

The aforementioned suggestions generate additional income for lenders in addition to the protocol, which is all stored in DAO Treasury. Because more recent integrations may result in higher fees, it gives Gearbox DAO financial incentives to integrate new features.

We call this revenue division power to GEAR stakeholders “Minimum Viable Tokenomics” because it’s the simplest model that generates natural use cases for GEAR. The DAO has the authority to select a mechanism that best suits the interests of the holders or stakeholders and then vote to adopt it for use in subsequent phases and sharing.